Exploring the concept of term life insurance, this introduction aims to provide a thorough understanding of this financial product. With a blend of informative insights and practical examples, readers will gain valuable knowledge on the topic.

The following paragraphs will delve deeper into the specifics of term life insurance, shedding light on its significance and benefits.

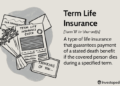

What is Term Life Insurance?

Term life insurance is a type of life insurance that provides coverage for a specific period, or term, of time. It offers financial protection to the policyholder's beneficiaries in the event of the policyholder's death during the term.

Fundamental Characteristics of Term Life Insurance

- Term length: Typically ranges from 10 to 30 years.

- Premiums: Generally more affordable compared to whole life insurance.

- Death benefit: Paid out to beneficiaries if the policyholder passes away during the term.

- No cash value: Term life insurance does not accumulate cash value over time.

Differences from Other Life Insurance Types

- Term vs. Whole life insurance: Term life insurance provides coverage for a specific period, while whole life insurance covers the policyholder for their entire life.

- Cost comparison: Term life insurance premiums are usually lower than whole life insurance premiums.

When Term Life Insurance is Recommended

- Individuals with financial dependents who want to provide protection for a specific period.

- Those seeking coverage for a specific financial obligation, like a mortgage or education expenses.

Key Features and Benefits

- Flexible term lengths to align with the policyholder's needs.

- Affordable premiums, making it accessible for many individuals.

- Provides a death benefit to beneficiaries if the policyholder passes away during the term.

How Does Term Life Insurance Work?

Term life insurance is a type of life insurance that provides coverage for a specific period of time, known as the term. During this term, the policyholder pays regular premiums to the insurance company in exchange for a death benefit that is paid out to the beneficiaries in the event of the policyholder's death.

Coverage Duration and Premiums

The coverage duration of a term life insurance policy can vary, typically ranging from 10 to 30 years. The length of the term chosen by the policyholder will impact the premiums they pay. Generally, the longer the term, the higher the premiums, as there is a higher likelihood of the policyholder passing away during a longer period.

Beneficiary Payouts

When the policyholder passes away during the term of the policy, the beneficiaries named in the policy will receive the death benefit. This payout is typically a tax-free lump sum payment that can be used by the beneficiaries to cover expenses, such as funeral costs, mortgage payments, or living expenses.

End of Term Life Insurance Policy

At the end of the term life insurance policy's term, the coverage expires, and the policyholder is no longer required to pay premiums. Some policies may offer the option to renew the coverage at a higher premium rate or convert it to a permanent life insurance policy.

If the policyholder passes away after the term has ended and the policy was not renewed, no death benefit will be paid out to the beneficiaries.

Types of Term Life Insurance Policies

When it comes to term life insurance, there are several different types of policies available to meet varying needs and preferences. Each type of policy has its own unique features, premium structure, and suitability for different individuals or situations. Let's explore the main types of term life insurance policies below:

1. Level Term Life Insurance

Level term life insurance is one of the most common types of term life policies. With this type of policy, the death benefit remains the same throughout the duration of the policy, while the premiums typically stay level as well.

This offers predictability and stability for the policyholder.

2

. Decreasing Term Life Insurance

Decreasing term life insurance, also known as mortgage protection insurance, is a policy where the death benefit decreases over time. This type of policy is often used to cover specific financial obligations that decrease over time, such as a mortgage or other loans.

3. Renewable Term Life Insurance

Renewable term life insurance allows policyholders to renew their coverage at the end of each term without having to undergo a medical exam. While the premiums may increase with each renewal, this type of policy provides flexibility for those who may need coverage beyond the initial term.

Additional Riders and Options

Many term life insurance policies offer additional riders or options that can be added to customize the coverage to better suit individual needs. Common riders include accelerated death benefit riders, which allow the policyholder to access a portion of the death benefit if diagnosed with a terminal illness, and waiver of premium riders, which waive premium payments if the policyholder becomes disabled.

Factors to Consider When Choosing Term Life Insurance

When selecting a term life insurance policy, several factors should be taken into consideration to ensure that the chosen policy meets the individual's needs and provides adequate coverage. Factors such as age, health status, coverage amount, and term length play a crucial role in determining the most suitable policy for an individual's circumstances.

Age

Age is a significant factor that influences the cost of term life insurance. Generally, the younger you are when you purchase a policy, the lower the premiums will be. This is because younger individuals are considered lower risk by insurance companies.

It is essential to buy a policy when you are young to lock in lower rates for the duration of the term.

Health

Your health status also plays a vital role in determining the cost of term life insurance. Individuals with pre-existing medical conditions or unhealthy lifestyles may face higher premiums or even be denied coverage. It is crucial to disclose all relevant health information accurately to ensure you are getting the right coverage at the best possible rate.

Coverage Amount

Determining the right amount of coverage needed is crucial when selecting a term life insurance policy. Consider factors such as outstanding debts, future financial obligations, and the needs of your dependents. It is recommended to choose a coverage amount that would replace your income for a specified period to ensure your loved ones are financially protected in the event of your death.

Term Length

The term length of the policy is another essential factor to consider. Term life insurance policies typically offer terms ranging from 10 to 30 years. Choose a term length that aligns with your financial goals and obligations. For instance, if you have young children, you may opt for a longer term to ensure they are financially secure until they become financially independent.

Comparing Quotes

Before choosing a term life insurance policy, it is essential to compare quotes from different insurance providers. This allows you to assess the coverage options, premiums, and terms offered by each company. By comparing quotes, you can ensure you are getting the best value for your money and the most suitable coverage for your needs.

Ultimate Conclusion

In conclusion, term life insurance offers a flexible and affordable way to protect your loved ones financially. By understanding its key features and considerations, individuals can make informed decisions when choosing a policy.

Essential Questionnaire

What is the difference between term life insurance and whole life insurance?

Term life insurance provides coverage for a specific period, while whole life insurance offers coverage for the entire lifetime of the policyholder.

Can I convert a term life insurance policy to a whole life insurance policy?

Some term life insurance policies offer the option to convert to a whole life policy, but it's important to check with your provider for specific details.

What happens if I outlive my term life insurance policy?

If you outlive your term life insurance policy, you can either renew it at a higher premium, convert it to a permanent policy, or let it expire.

Are term life insurance premiums tax-deductible?

Term life insurance premiums are generally not tax-deductible, but the death benefit is usually tax-free for the beneficiaries.

{kind=link}